Market selloff what does it mean? Why Europe is attractive right now

If investors look at flows/technicals of fixed income markets over the past year, there has been significantly more investment flow into investment-grade, not high-yield, as well as more into non-US equities than US equities

In further analyzing investor risk appetite and investment themes we have seen significantly more money going into higher quality assets, such as government bonds, investment-grade bonds, and large cap equity, and much less going into riskier assets such as high yield, emerging markets, and small-cap stocks.

With this makes us think is that we are not near the end of the boom market, as most booms or bubbles feature investors taking more and more risk with lower and lower quality assets near the end of the boom & bust cycle.

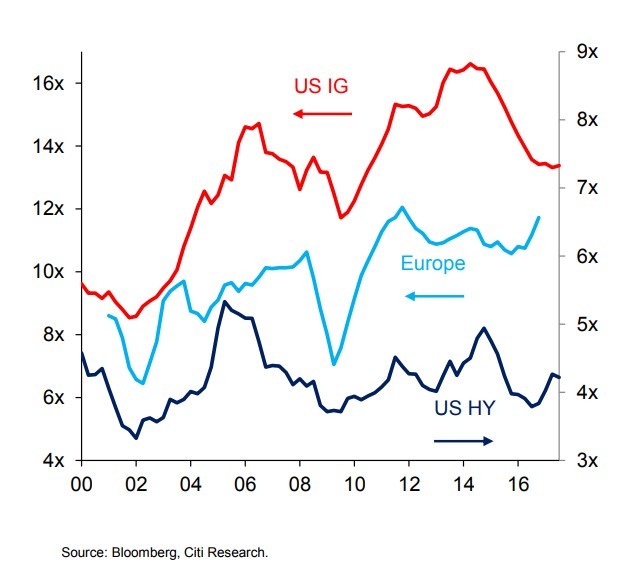

In the chart below, you can clearly see that the interest coverage ratio of the US investment grade market has been coming down, this means that leverage ratios have been going up as the absolute amount of issuance has been increasing.

Not at all the case with Europe where we have seen interest coverage ratios improving, Europe and the US are therefore at different points in their credit cycles.

We believe that too much money chasing too few assets has caused the safe low volatility higher-quality trades to outperform due to the technical’s of too much money chasing too few trades. What this means is that we are likely to see a rotation into more interesting higher risk smaller capitalization trades that are more global in nature such as Europe and emerging markets, and a rotation out of US centric trades such as US S&P 500 and Dow Jones, US treasuries, and investment-grade

Should investors be worried about inflation?, Well it looks like bonds are way ahead of real inflation, as demonstrated by this graph showing nominal inflation as compared to US 10 year bond yields, we remain mixed in our concern — wage inflation could cause an acceleration of overall inflation due to tight labour markets, however emerging markets will and can pick up the slack in manufacturing and services if prices and wages rise too quickly in the states. The swing factor is the overall inflation rate and tightness of the labour market in emerging markets principally China

Europe Looks Cheap

If investors look at the past 12 months very interesting trends are obvious. The first major trend is that the US market has been overbought relative to European markets, the second is that a weaker dollar has made it very attractive to buy these assets and that if inflation increases we would expect the dollar to strengthen, which would naturally reverse the overbought condition on US markets.

This leads us to believe that in the next 12 months Europe and emerging market assets will be compellingly cheap relative to US markets.

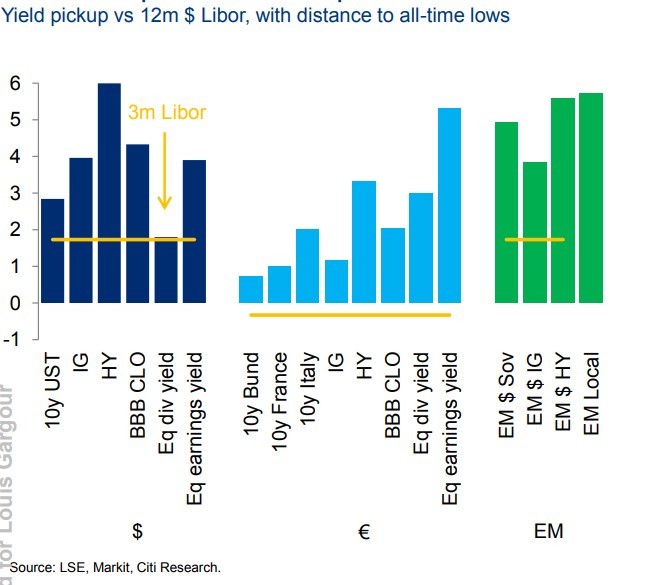

In fact if you look at the below chart you will see that aside from government bonds in Europe, high-yield and equities are undervalued, underappreciated and very far from their all-time lows whereas the dividend yield of the US market is at its all-times tight.

This leads us to the following conclusion: The selloff that we had just seen is a result of inflation expectations rising in the US, as well as the equity and fixed income markets both enjoying a two-year bull run with no interruption. This has made those two asset classes rich relative to other countries, therefore investors should assume that the following is true….

1- Inflation may rise quicker than anticipated in the US

Recommendation- stay away from US government and investment-grade bonds in the next 12 months

2- Equity market growth has been supported by earnings growth in the US, valuations in US equity markets are at all-time highs, and dividend yield at at all time lows

Recommendation – Look to other equity markets which are cheaper and earlier cycle these include Europe and emerging markets

3 – How will credit respond to the rise in rates

Recommendation – Lower quality credit will benefit from global growth just like equities. Therefore non-US lower quality credit is a very interesting asset class in an environment where you combine growth, and slowly rising inflation

4 – What types of bond trades should investors have in portfolios

Recommendation – Investors want to limit duration and convexity but receive a steady income as opposed to capital gains and the associated volatility, therefore lower rated instruments are an overweight as are floating rate instruments

Mr. Gargour is the chief investment officer of LNG capital LLP a London-based investment firm. LNG adopts an active long/short approach focusing on European markets.

If you would like to get in contact please feel free to write or call us. You can reach client relations at [email protected] or +442078393456

ShareShare Market selloff what does it mean? Why Europe is attractive right now

LikeMarket selloff what does it mean? Why Europe is attractive right nowCommentShareShare Market selloff what does it mean? Why Europe is attractive right now